Shubham Sanghavi, Senior Consultant, and Rathin Sarmah, Consultant, at Avalon Consulting explore how India’s growing water crisis is emerging as a critical business challenge, with significant implications for economic growth, industrial operations, and long-term sustainability. The article examines the structural drivers of water scarcity and the need for businesses to adopt a more resilient approach to water management.

It also highlights the role of wastewater reuse, desalination, technological innovation, and public-private collaboration in strengthening water security. As climate risks and resource constraints intensify, water resilience is becoming a strategic priority for business leaders seeking sustainable growth and operational continuity.

India’s Water Crisis: Turning Scarcity into Opportunity Through Private Participation and Innovation

India is home to 18% of the world’s population, with access to a measly 4% of the planet’s actual freshwater. According to the latest data from NITI Aayog (2023), our “water bank account” is draining fast. In 2021, the per capita availability was at 1,486 cubic meters which is well below the global threshold of 1,700 cubic meters and by 2031, we are looking at it dropping further to 1,367 cubic meters.

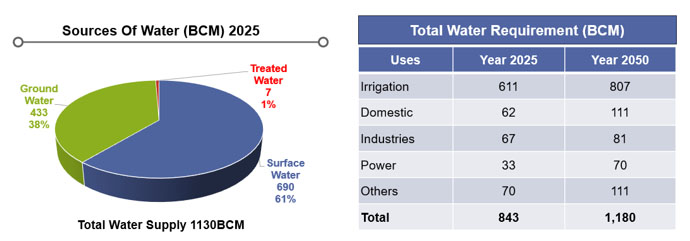

India relies almost entirely on surface water (61%) and groundwater (38%), while ignoring treated wastewater. Our thirst for groundwater, especially in the agricultural belts of Punjab, Rajasthan, and Haryana, is reaching a breaking point. We are using up reserves at an unsustainable pace far faster than nature revives it.

However, despite its potential and our shrinking freshwater reserves, treated water makes up a tiny 1% of our usage. This represents a massive opportunity for both governments and private players to invest in water treatment infrastructure and technology.

There are two ways to treat wastewater.

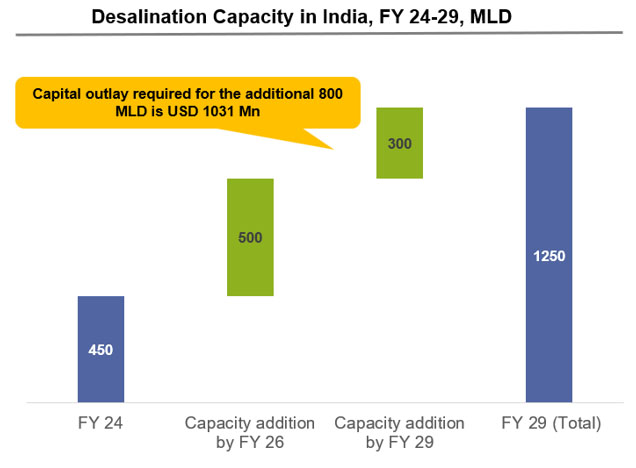

Desalination is the process of removing dissolved salts and impurities from water to make it suitable for human consumption and industrial use. In India we have a capacity of 450 MLD and is expected to reach 1250 MLD by 2029.

In India, only Tamil Nadu and Gujarat are promoting desalination with 350 MLD capacity in Tamil Nadu and 100 MLD capacity in Gujarat. Other states like Andhra Pradesh and Maharashtra are trying to follow in their footsteps. With current and planned capacity, the output is expected to reach only ~0.5 BCM, which is negligible relative to the overall potential. There is significant headroom to scale this up to ~20 BCM with targeted investments and capacity expansion

However, the key challenge is that it is incredibly expensive and risky. If we were to meet 2% of our needs with desalinated water (~20 BCM), then the estimated capex cost would be ~ USD 80 Bn. (INR 7.2 lakh crores). At the current water procurement price of municipalities breakeven can be expected only after 8-10 years. Adding to this is the uncertainty around membrane development which will lead to further investments in capex.

Innovation and government support are key to ensuring this sector moves forward. There are new developments in membrane technology, such as longer-lasting graphene-based membranes, decentralized containerized treatment facilities for industrial applications, and AI-based monitoring systems. These are expected to reduce the cost further, making desalination even more feasible.

Government support and PPPs are the way forward. The Tamil Nadu government is currently leading the charge, making it mandatory for industries to switch to recycled water by 2027. When coupled with financial support mechanisms like Viability Gap Funding, these massive projects finally start to look less like a burden and more like an attractive investment. There are promising examples. Chennai’s Nemmeli plant is pumping out 100 MLD of desalinated water, which they are operating under DBOOT model with VA Tech Wabag and IDE Technologies with commitment from the government to procure 90 MLD.

Sewage Treatment also provides adequate scope for development. India’s class 1 and 2 cities generate ~72,500 MLD waste while the installed treatment capacity is of ~32,000 MLD. Central urban development schemes such as Jal Shakti Abhiyan, Swachh Bharat Mission, Atal Mission for Rejuvenation and Urban Transformation (AMRUT), Smart Cities Mission and Namami Gange have been put forth to tackle the sewage treatment issue and emphasise the reuse of wastewater for various purposes.

The cost of setting up a sewage treatment plant is relatively lower than that of a desalination plant but has its own challenges. Sewage treatment projects face challenges such as limited bidding transparency, labour and supply chain disruptions, price pressure from unorganized players, poor equipment quality, delayed municipal payments, variation in sewage inflow and quality, and consumer resistance to paying reasonable water tariffs.

Globally Singapore has set an example. Their “NEWater” program handles 40% of the nation’s demand. They didn’t just build the tech, they won over the public, proving that “reclaimed water” can become a national brand if you communicate it right. Israel too recycles a staggering 90% of their sewage and they have made their food supply almost entirely independent of the weather.

At the end of the day, transforming India’s water needs to be done jointly in the form of Public-Private Partnerships (PPPs). The government sets the rules, provides the funding incentives, and guarantees a market, while private companies bring the actual “boots on the ground” the innovation, the capital, and the day-to-day expertise. India’s water crisis is a massive wake-up call, but it’s also an opportunity for a total system reset. The government along with the private sector can jointly work towards turning sewage into a resource and the ocean into a lifeline.

Shubham Sanghavi

Shubham Sanghavi is a senior management consultant with extensive experience working with clients across various industries, including automobile, chemical, consumer, and technology. He has successfully assisted clients in areas such as market entry, performance improvement, and transformation. Before joining Management Consulting, Shubham earned his MBA from NMIMS, Mumbai, and his B.Tech from Amrita School of Engineering, Bangalore

Rathin Sarmah

Rathin Sarmah is a management consultant focused on driving growth and transformation through Market Assessment, Go-to-Market Strategy, and Organizational Transformation. He has worked with clients across automobiles, chemicals, and FMCG helping leaders size opportunities, sharpen strategic choices, and translate plans into clear execution roadmaps. Rathin brings a structured, problem-solving mindset to every engagement, with a strong interest in how evolving customer needs, competitive intensity, and operating model shifts are reshaping modern businesses. Before joining Management Consulting, Rathin earned his MBA from XIMB, Bhubaneswar and his BBA from Symbiosis Center for Management Studies Pune