Bibhu Prasad, Associate Vice President, and Raghav Bansal, Consultant at Avalon Consulting shared their views on India’s aviation sector in the article “Breaking the Duopoly: Can New Airlines Really Fix India’s Aviation Fragility?”

They highlighted that India’s aviation market remains highly concentrated, with IndiGo and Air India collectively controlling around 90% of domestic market share, making the sector vulnerable to large-scale disruptions during operational crises. While the entry of new airlines may improve resilience at the margins, the article notes that structural challenges such as high fuel costs, slot scarcity, and capital-intensive operations continue to limit meaningful competition. Further, they suggested that India must pursue deeper structural reforms including ATF rationalization, fleet support for mid-sized carriers, and stronger competition oversight to build a more resilient and diversified aviation ecosystem.

India experienced one of its worst aviation crises in December 2025. Indigo cancelled about 2,500 flights in three days, leaving 300,000 passengers stuck at airports all over the country. India’s air travel system stopped working, turning what should have been a normal trip into a chaotic national emergency. More concerning than operational shortcomings, the crisis exposed the vulnerability of a two-player market.

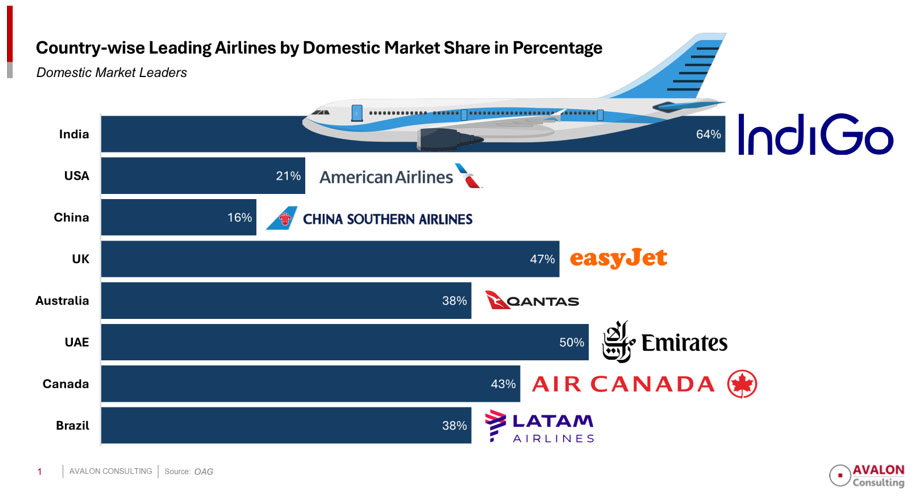

Together, IndiGo and the Air India Group hold about 90% of the domestic market in India. Air India Group owns ~27% of the market, while IndiGo alone operates 429 aircraft and commands a 64% share. The remaining competitors have marginal market shares, such as SpiceJet (4%) and Akasa Air (4.7%). Like many other industries in India currently, civil aviation is clearly a duopoly.

The Duopoly Doesn’t Exist in Major Markets

This extreme concentration stands in stark contrast to mature aviation markets. In the world’s largest aviation market, the USA, the market share between American Airlines, Delta, Southwest, and United ranges between 16% to 21% for each. These top four carriers together have about 75% of the market, but no one airline is massively dominant. Similarly, in China, the “big three” state carriers are China Southern (16%), China Eastern (14%), and Air China (~11%). They together operate majority of domestic capacity, leaving substantial room for other regional players. Both markets exhibit healthy competition that provides resilience as compared to India where Indigo alone has 64% market.

India’s 90% duopoly concentration means passengers have virtually no alternatives when disruptions occur. The IndiGo crisis demonstrated this starkly. Competitor airlines briefly added flights but lacked the scale to meaningfully relieve pressure.

The Government’s Response: Three New Entrants

Three airlines Shankh Air, Al Hind Air, and FlyExpress were granted No Objection Certificates (NOCs) by the government following the crisis. The Ministry of Civil Aviation, made it apparent that the approvals were intended to aid in resolving the duopoly issue and expediting entry of new airlines to reduce flyer excessive dependence on just 2 players. The rumour quickly spread that new rivals would finally challenge IndiGo and Air India by enhancing service, cutting costs, and strengthening the system’s dependability. But a close look at the fleet’s capacity and passenger projections shows a sad truth.

| Airline | Aircraft in Service as of March 2026 | Projected Fleet by End of 2029 | Comments |

|---|---|---|---|

| Shankh Air | 3 | 20-25 | Started with 3 A320s in March 2026; plans to add 2 more by July-August 2026 |

| Al Hind Air | 0 | 7+ | Not yet operational. Plans to start with 2 ATR aircraft, scaling to 7 ATRs |

| Fly Express | 0 | 20 (estimated) | NOC granted but no specific inducted aircraft disclosed yet. Limited public information on fleet plans, but early reports suggest a target of about 20 aircraft within 3 years |

| TOTAL | 3 | 47-52+ | Only Shankh Air currently operational with confirmed aircraft in service. |

Initial capacity is approximately 4,320 seats per day, assuming an optimistic combined active fleet of six aircraft by the end of 2026, with four daily flights per aircraft and 180 seats per flight. That equates to about 3,670 passengers per day at 85% PLF. The initial share of the new trio would have been less than 0.22% in 2025 since the domestic market in India handled about 15–16 lakh passengers every day. Even at aspirational projected fleet size of about 50 aircraft by 2029 for all these three airlines combined (considering they become operational on time and global macroeconomic factors don’t disrupt their growth and operations), ~23,000 seats/day or ~1.2% market share which is still negligible versus IndiGo’s 64%. DGCA/MoCA projections eye 400 million passengers by 2028-29; new airlines would find it difficult to attain 1% of the market amid capital hurdles and slot scarcity.

Why Airline Survival is So Difficult in India

Since 1994, over 20 airlines have shut down in India. These include major pan India airlines like Go First in 2023, Kingfisher Airlines in 2012, and Jet Airways in 2019, among many regional ones. The INR volatility in relation to the USD increases lease and debt obligations, fare caps restrict pricing power, and ATF accounts for 30–40% of operating costs. There are many carriers in the graveyard who miscalculated India’s difficult operating conditions within the aviation space.

The three new entrants will face similar headwinds, compounded by disadvantages in slot allocation at congested airports, lack of brand recognition, the incumbents’ overwhelming economies of scale. The rise in ATF prices due to the ongoing war in the Middle East will be an additional overwhelming challenge. Even established players like SpiceJet, despite years of operations and an extensive network, struggle to maintain viability in the current scenario.

What Must Be done on our Path Forward

The December 2025 IndiGo crisis was a wake-up call that exposed the perils of duopoly. But hyping micro-entrants risks false hope. Shankh, Al Hind, and FlyExpress add resilience on the fringes but won’t dent 90%+ dominance soon. True competition demands bolder moves: fleet subsidies for mid-tier carriers, antitrust scrutiny on slots/pricing, and ATF rationalization. State governments can play their part through Viability Gap Funding. Without these, India’s aviation ambitions risk remaining captive to two giants – unlike the matured models in the US and China. India handled ~240 million passengers in 2024; growth to 400 million by 2030 requires diversified capacity, not token players.

Bibhu Prasad

Bibhu Prasad is an Associate Vice President at Avalon Consulting. He is a consulting professional with over 10 years of diverse experience across Growth Strategy, Performance Improvement, and Digital Transformation across Metal and Mining, Agribusiness, Chemicals, FMCG, Automotive and Transportation sectors.

Raghav Bansal

Raghav Bansal is a Management Consultant at Avalon Consulting, specializing in aviation, automotive and chemical sectors. He has prior experience in digital transformation, customer satisfaction research for Indian OEMs, and process improvement projects. Bringing a structured problem-solving mindset to every engagement, Raghav has deep interest in how market dynamics shape modern business strategy.