Raghav Bansal, Consultant at Avalon Consulting, shared his views on India’s ageing population in the article “Understanding Consumption Behaviour of the Ageing Population: India’s Silent Growth Engine.”

He highlighted that India’s rapidly growing elderly population is emerging as a significant consumption driver, creating a large “silver economy” opportunity across sectors such as banking, retail, hospitality, electronics, and healthcare. The article notes that ageing consumers prioritize trust, simplicity, security, human interaction, and long-term value over speed and novelty, yet remain underserved by today’s youth-centric business models.

Further, he suggested that companies must redesign products, services, and customer journeys around accessibility, trust-rich interactions, and life-stage realities to effectively cater to this expanding and increasingly connected consumer segment.

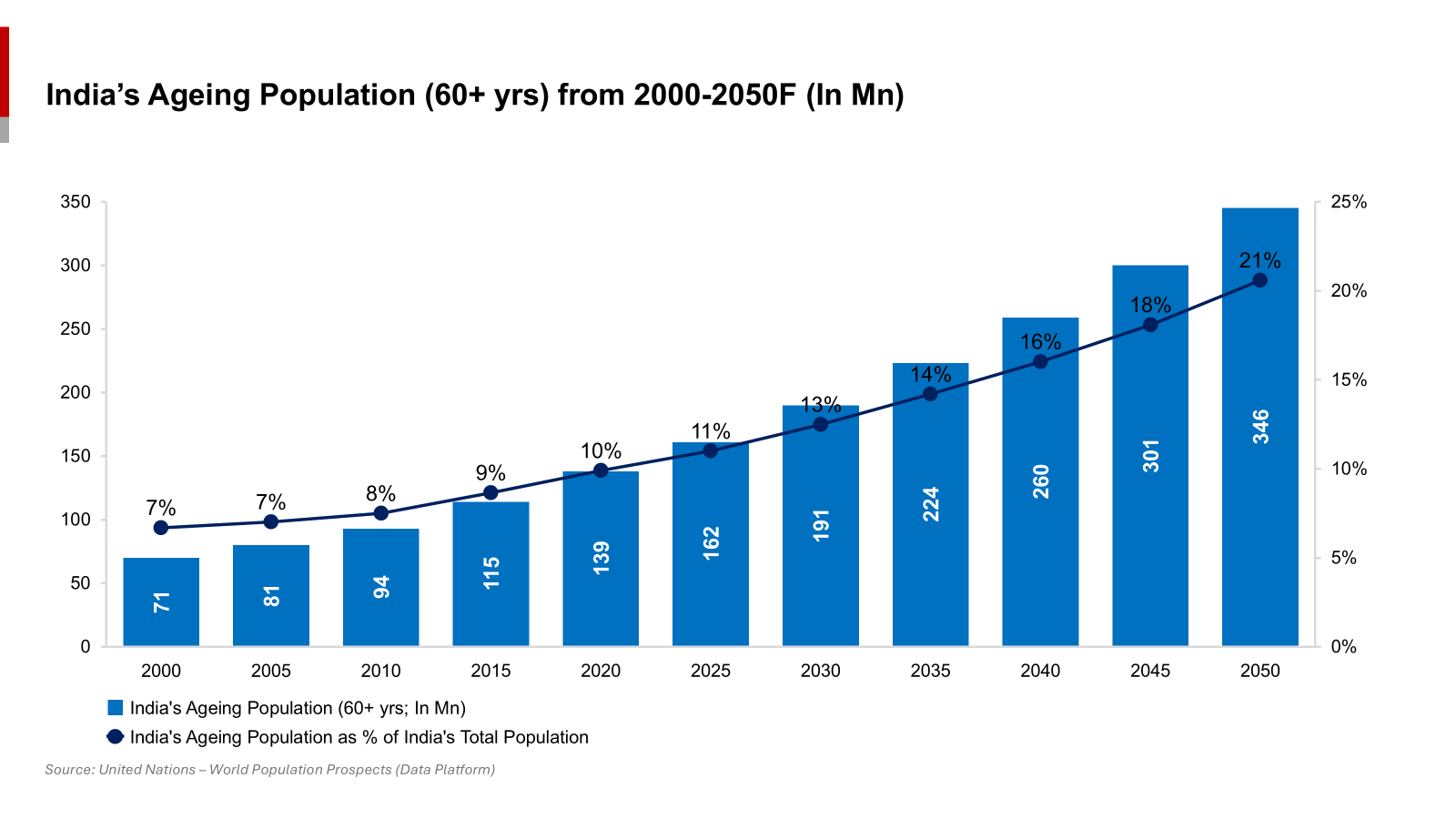

India, with a median age of 28 years compared to 38 years in China and 48 years in Japan, is one of the youngest countries in the world. The share of elderly Indians is rising fast, however. With 12% of the population being elderly as of now, this number is projected to reach about 230 Mn people in 2036 and 345 Mn people by 2050 (about 20% of the population). This powers a “silver economy” positioned for multi-fold growth. By 2100, 1 out of every 4 people in India will be over 65 years of age. Thus, ageing consumers in India are no longer a marginal segment. They are a critical demand driver that businesses can no longer afford to overlook.

India – A Young Country with an Ageing Edge

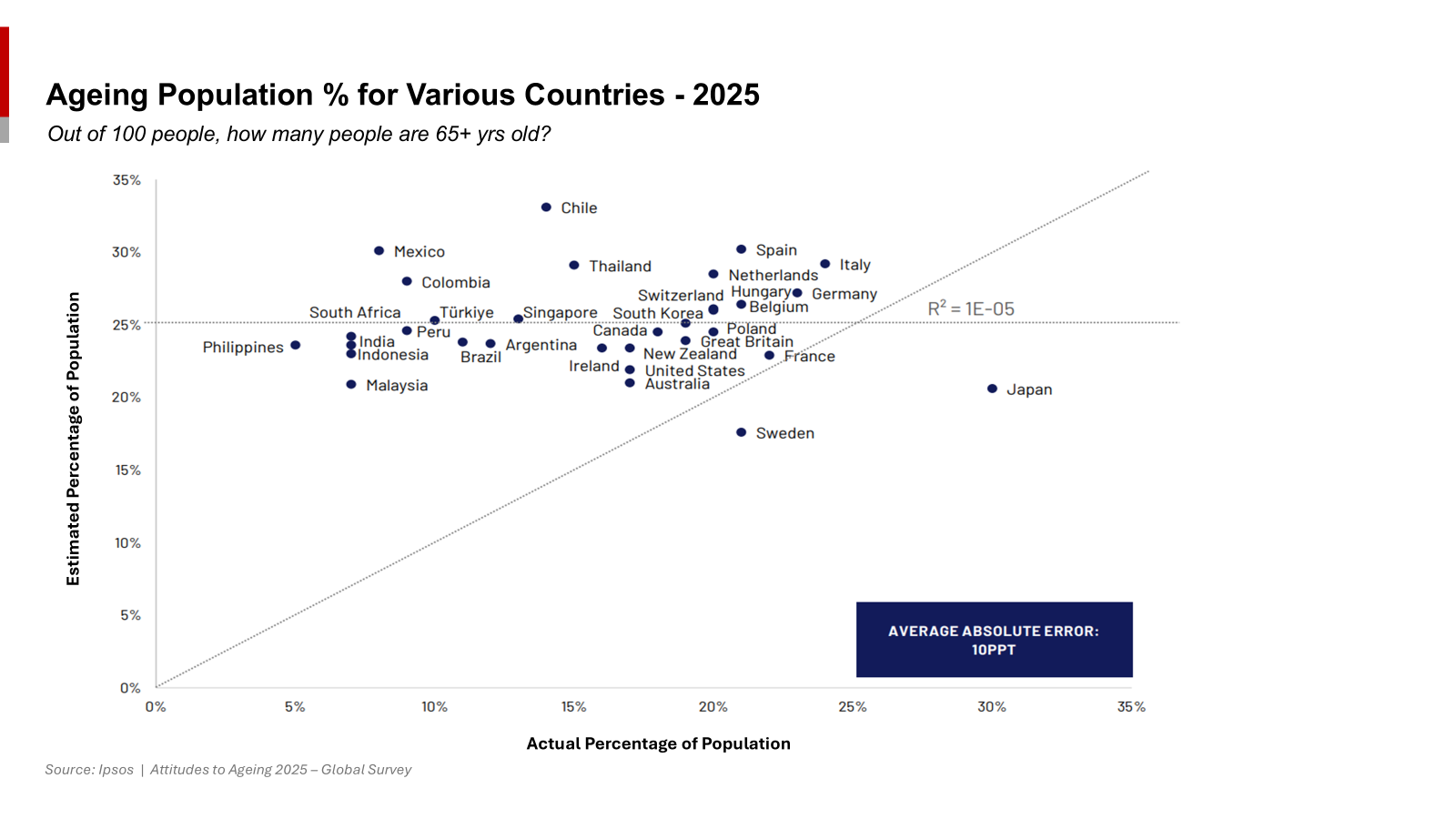

India’s demographic dividend is expected to last int the 2040s, with a large working-age population and a median age still in the late twenties. The same is also reflected in the 2025 ageing population percentage numbers of India compared with other countries.

However, as seen in economies like Russia, which is expected to face labour shortages by the early 2030s as large cohorts retire, the transition from “young” to “ageing” can be sharp and economically disruptive if not anticipated. Rising cost of living and life expectancies are not helping. This large percentage of population are nearing retirement and are either dependent on children or are looking for alternate employment since savings are insufficient to meet demands. For India, building an economy that understands and serves older consumers is part of future-proofing growth, not just social policy.

When Channels Assume Youth

Most customer-facing channels in India—apps, branch formats, store designs, call centres, even loyalty programs—are implicitly designed around younger, digital-first, high-churn customers. From friction-heavy IVR menus in banks to dark-store grocery apps and QR code–driven restaurant experiences, the default user persona is tech-comfortable, time-poor, and willing to self-serve. Older customers, by contrast, often prioritise clarity, personal assistance, and relationship continuity over speed or novelty, which today’s sales models frequently under-serve.

This is not because seniors are offline. Markets such as Japan break the myth that seniors are digitally handicapped with smartphone penetration of above 80% with 90% of people in their 60s using internet. Evidence from China shows that digital use among older adults improves lifestyle quality and social participation. The real gap is not connectivity, but whether products and journeys reflect older consumers’ values and risks.

What Drives the Ageing Consumer?

Across sectors, ageing consumers tend to anchor their decisions based on a combination of factors like trust, perceived security, simplicity, long-term value, health and family considerations.

- Banking and payments: Older consumers are sensitive to fraud risk, hidden charges, and complex UI. They value in-person reassurances, clear costing structures, and human help at key interaction endpoints.

- Retail and consumer electronics: Ageing consumers value reliability, after-sales service, warranties, and ease of use. Cutting-edge features are of low priority. Clear communication and demonstrations can prove to be as important as discounts.

- Hospitality and travel: Safety, accessibility, predictability, and respectful service outrank hyper-personalised upsells. Package clarity and the ability to speak to a human when plans change are pivotal.

- Food & beverage: Health, hygiene, dietary needs, and familiarity are the most common factors that guide consumer choices for this cohort. They have now begun to drive premium demand for quality and experience in the F&B sector now.

Various patterns around consumption behaviour can be inferred from these commonalities – a need for trust-rich interactions, low cognitive load, consistent human support, and products calibrated to life-stage realities rather than youth trends.

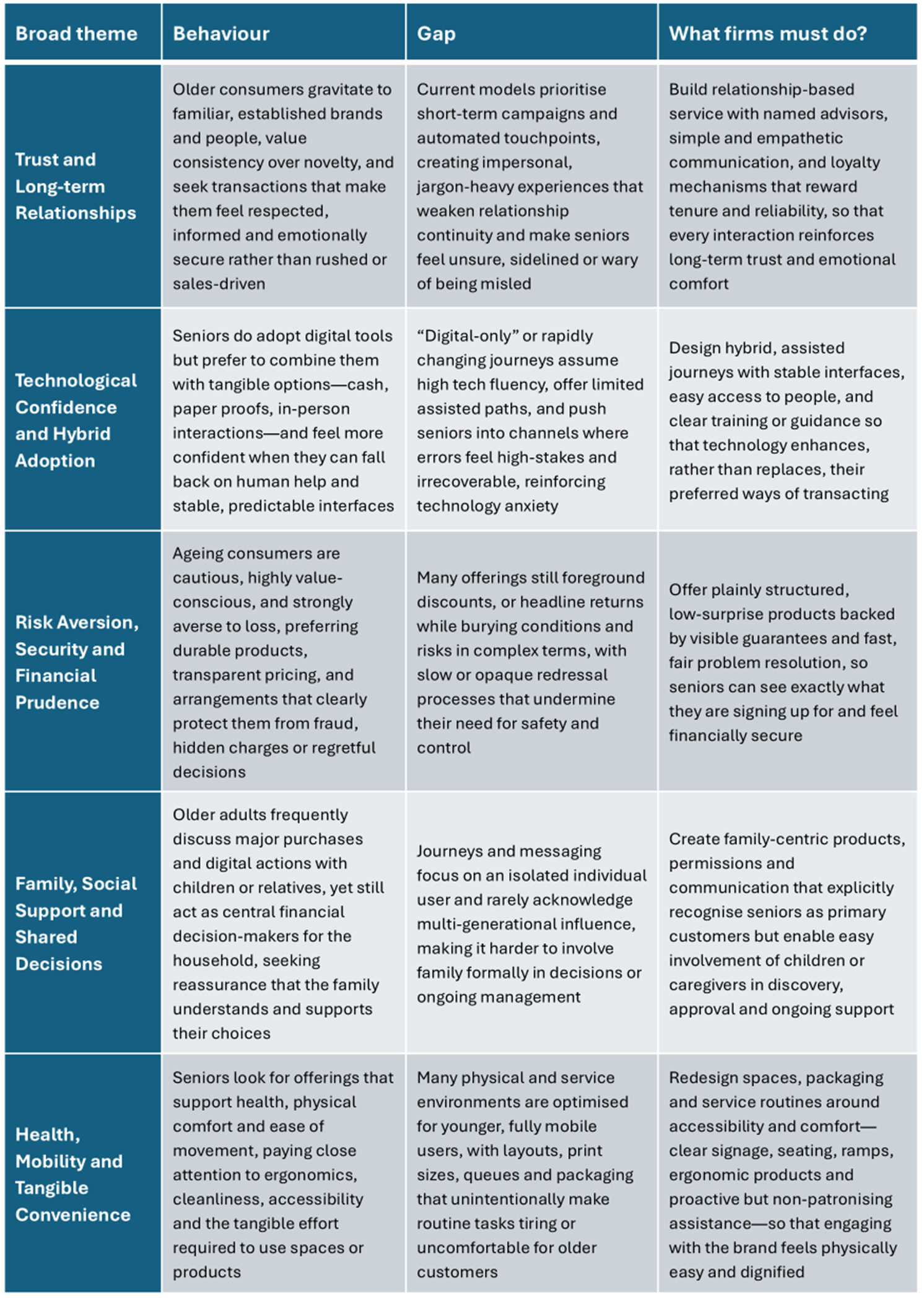

Ageing Consumers: Behaviour, Gaps, and What Firms Must Do

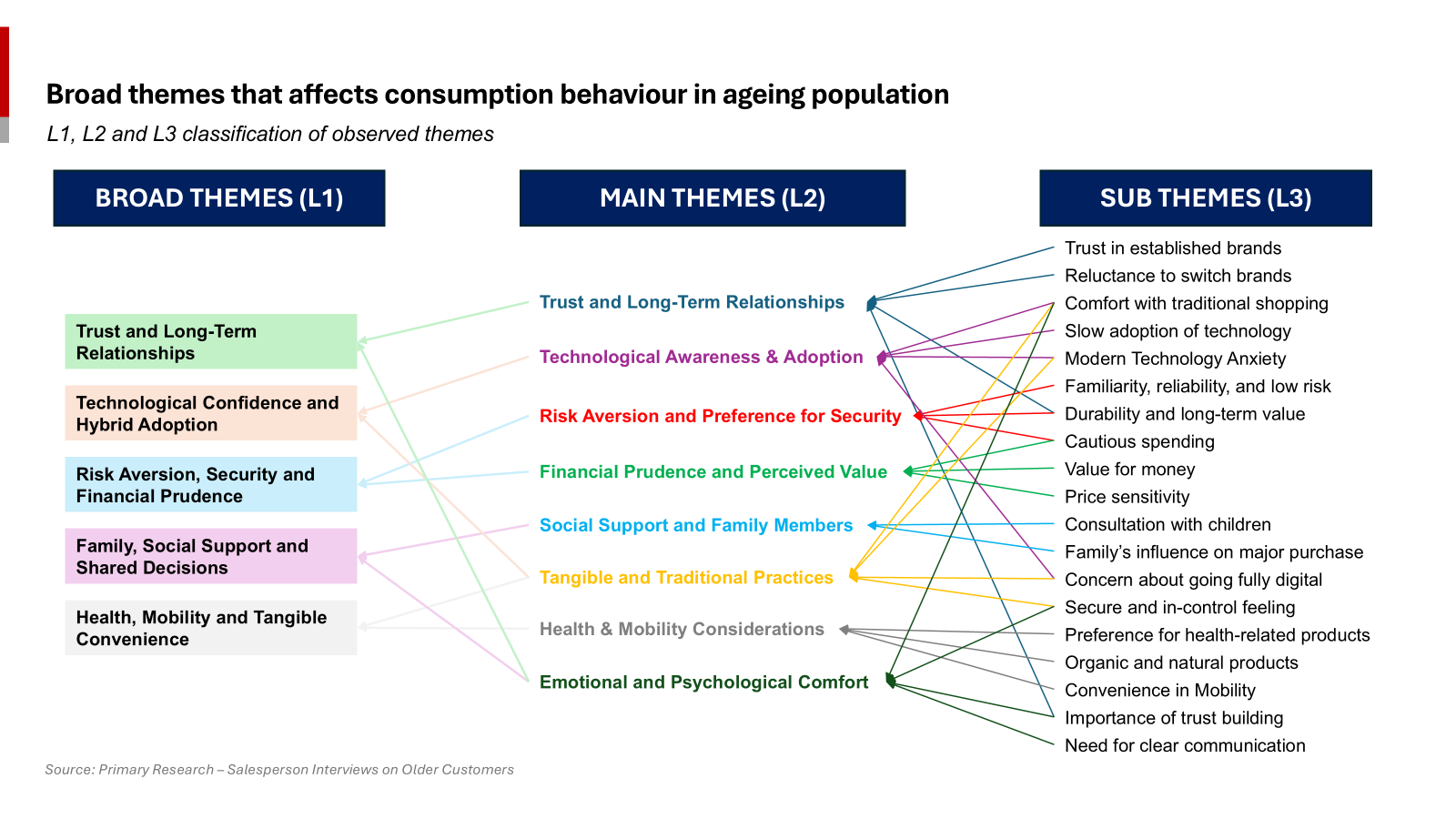

All the sub-themes and emerging themes can be brought together under five broad themes that define the gap and the opportunity with ageing consumers in India.

Ageing Indians are not laggards, they are an under-served, asset-rich, and increasingly connected cohort. Many of them also happen to be major decision makers for their sub-18-year-olds. Their choices will shape demand in banking, retail, hospitality, electronics, F&B and other sectors over the next two decades. Companies must re-anchor their models around trust, security, human connection, and accessible design, to be best placed to serve this silent growth engine of India’s consumption story.

Raghav Bansal

Raghav Bansal is a Management Consultant at Avalon Consulting, specializing in aviation, automotive and chemical sectors. He has prior experience in digital transformation, customer satisfaction research for Indian OEMs, and process improvement projects. Bringing a structured problem-solving mindset to every engagement, Raghav has deep interest in how market dynamics shape modern business strategy.